IDEX Online Research: Polished Diamond Prices Flat in October

November 04, 13

(IDEX Online) – The IDEX Online Polished Diamond Index was nearly flat in October, as most items either declined or increased slightly during the month. The IDEX Online Polished Diamond Index averaged 132.7 in October, increasing by 0.1 percent compared to September.

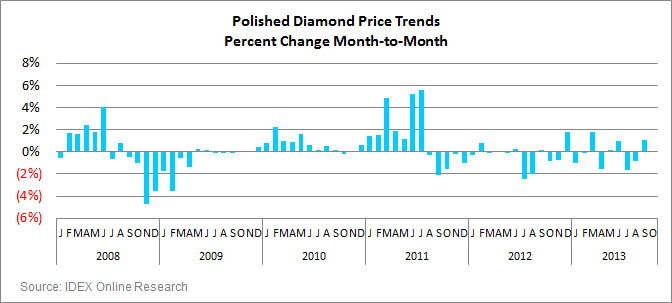

After a strong 1-percent month-over-month increase in September, which mainly reflected the confidence wholesalers felt after returning to work from their August vacations, overall polished diamond prices held steady in October.

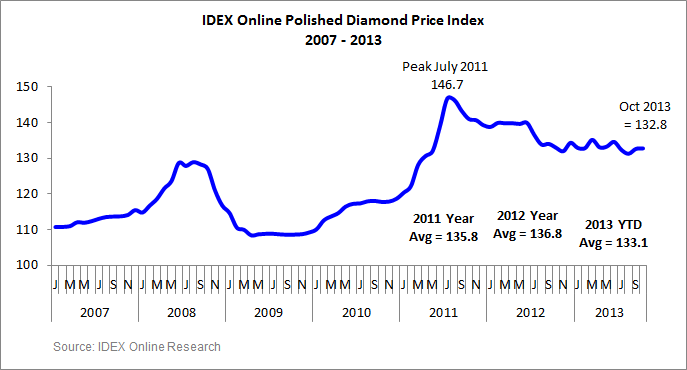

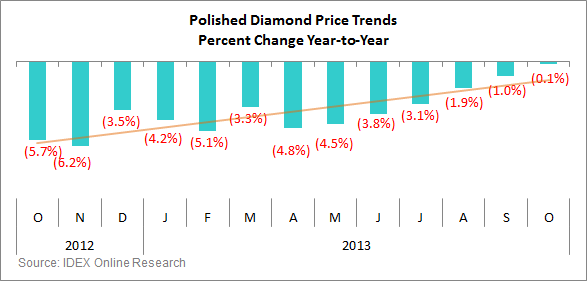

As the loose wholesale diamond sector prepares for November-December holiday demands, traders held strong the prices of many key size items. On a year-over-year basis, the index declined 0.1 percent. The overall monthly year-over-year decline in the Index has been shrinking continuously since April when it stood at -4.8 percent. In the first half of 2012, polished diamond prices were relatively high, and declined in the latter part of the year.

As the gap is closing, polished diamond prices are now back to their fourth quarter of 2012 levels. Overall, average prices have declined by 0.1-percent since January 2013.

It is too early to see what impact the Diwali vacation time will have on prices in the short-term, however historically, or at least since 2008, wholesale prices in November tend to be steady. Only in December do prices react strongly to holiday season demands in the U.S. and elsewhere, as last-minute orders cater to special purchases by consumers.

The flat index in October levels out somewhat the seesaw affect we have been witnessing in prices over the past year, however, it does not signal an end to it. If anything, it demonstrates a relatively steady level of prices, even as the November-December holiday season rolls in.

Is this near plateau in prices in 2013 evidence that polished diamonds have found their “right” price? Not necessarily. The “right” price is one that gives both sides of the transaction – retailers and jewelry makers on one side, and loose manufacturers on the other – a decent room for profit. It is not clear that is the case here. Current prices are a thin ledge requiring a perilous balance between the deep end of loss and the steep wall of rough diamond prices.

It is not that prices should increase to create a decent margin for sellers – because it will then be too high for consumers. Rather, it is rough diamond prices that need to pull back to make room for everyone down the value chain.

Recently, miners have eased rough diamond prices by a few percentage points, but this is too little, too late. Prices need to cool further, to allow wholesalers to offer discounts where needed, and for consumers to have diamonds as a viable alternative to other attractive holiday offerings.

The leading reason for the lower prices in the past year is large supplies and limited demand. Manufacturers polished a large overhang of rough diamonds and are now ready to move the big stock of polished goods to retailers.

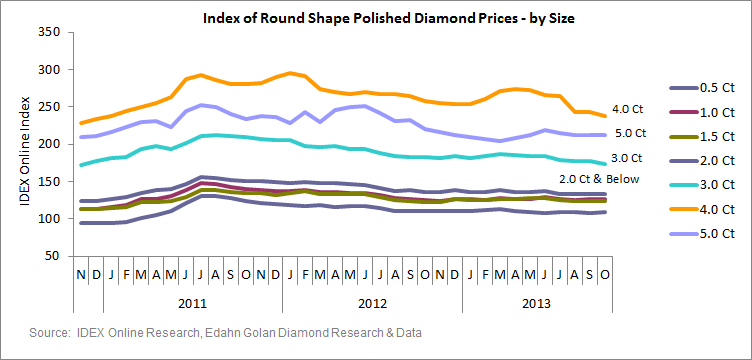

Round Shape Diamonds Prices by Size and Shape

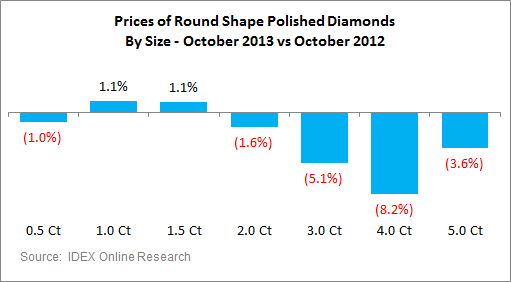

The index of 1-carat rounds increased by 1.1 percent in October on a year-over-year basis, as did the price index of 1.5-carat rounds. The average price of 4-carat rounds, a very price active item, dropped 8.2 percent during the month.

Other key round diamond sizes declined. Half-carat rounds lost 1.0 percent, 2-carat rounds declined by 1.6 percent while the price index for 3-carat rounds lost 5.1-percent in October.

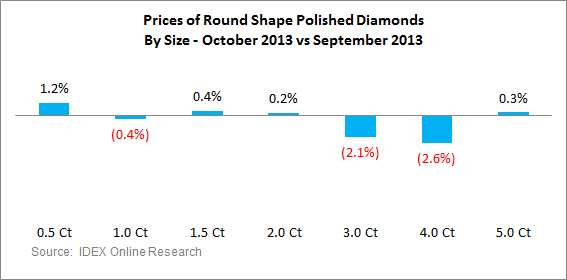

On a month-over-month basis, round goods demonstrated a mixed performance in October. The important 1-carat goods declined by 0.4 percent, while 2-carat rounds eased up by 0.2 percent compared to September. The surprise performers of the month were the half carat goods, which increased by a very robust 1.2 percent.

Three and 4-carat rounds lost on average more than 2 percent of their price in October compared to September For the 3-carat items, this is the fourth consecutive month of price declines, losing 6 percent of its price since July.

Prices of Princess-Shape Diamonds Fall

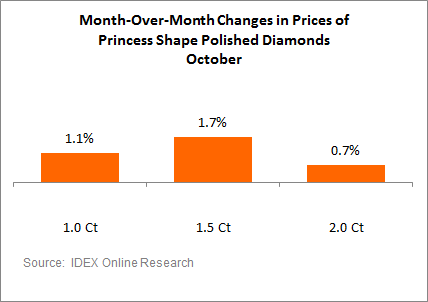

The key size Princess-shape increased for a second month in a row on a month-over-month basis. This is an encouraging sign after the price dip in May, the small recovery in June, and the decline in August.

All three key sizes, 1, 1.5 and 2 carat Princess shape goods made a decent price gain of about 1 percent. These gains resemble the price hikes seen earlier in the year, and beg the question - are these goods back in strong demand for the holiday season.

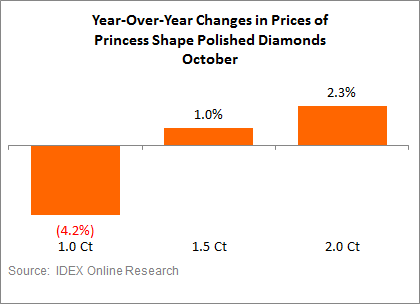

On a year-over-year basis, the price fluctuations are more significant. The average price of 1-carat Princess Shape diamonds declined for a second month, down by 4.2 percent.

The 2-carat Princess Items, increased by 2.3 percent while the 1.5-carat items gained 1 percent, compared to their October 2012 prices.

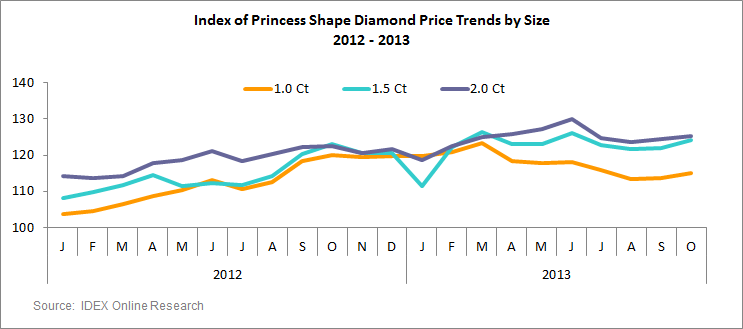

The long-term trend of Princess shape diamonds in the three key sizes shows that they have had an extended period of price increases, not wavering until recent months. Princess shape goods were a price-depressed item with limited demand until jewelers turned to them in response to high round diamond prices. The rise in prices followed the swelling demand.

Long-Term Historic Trend

After steadily increasing from the 2009 crisis, developing into runaway prices in the first half of 2011, the IDEX Online index peaked at 146.7 in July 2011, and has been on a general downward trend that moderated into flattish prices in 2013 to date. In the last few months, the IDEX Online Polished Diamond Index has been moving within a narrow band averaging about 133 since January 2013.

Outlook

We are continuing to hold to the cautious outlook we have expressed in the past months. The price fluctuations in recent months demonstrate that the diamond pipeline is still struggling to find a clear direction.

The weakening of the Indian rupee against the U.S. dollar has seriously harmed the Indian diamond sector and it is still struggling to get used to the depreciating rupee. The Indian sector’s foreign currency financing is rupee based, which means that if the rupee is worth less, their foreign currency allocation decreases. In an industry operating on single-digit margins, the double-digit drop in the value of the rupee is devastating.

The economic havoc in India is not expected to change dramatically until the general elections, and the depressed rupee is not expected to revive against the dollar in the near future.

In the U.S., retailers enjoyed a good run in the first half of 2013, and this trend continued into the third quarter. A rising stock market in the U.S. is good news on the consumer front. The S&P 500 increased by more than 23 percent in the first 10 months of 2013, outpacing the 19-percent forecast by many economists for the full year.

Swelling stock market prices mean that many Americans will have deeper pockets for discretionary expenses in the November-December holiday season and diamond jewelry will benefit from this spending.

Solid demand from China, despite the recent slowdown in demand growth, provides additional reasons to expect at least a moderate improvement in demand in the coming months. However, lackluster demand from Indian consumers, hurt by the weakening rupee, is dampening the global demand outlook.

With global stock markets continuing to rise, an improving U.S. economy, and expectations that the slowing Chinese economy will not deteriorate further, we expect polished diamond prices to increase in the long-term, especially with the improving Japanese economy, which is still a leading diamond-consuming market.